This is just a brief update to my previous post. I have to be careful what I write because I’m being watched. No, honestly, this is not paranoia, certain people will be reading this very carefully.

Therefore I hope you will understand that I have to be cautious, avoiding the injudicious phrase, the unintended calumny, otherwise certain persons down west will again be scuttling to £260-an-hour Ms Tracey Singlehurst-Ward of Hugh James Legal.

A BIG FAT I.O.U.

To recap . . . Mill Bay Homes is a ‘subsidiary’ of Pembrokeshire Housing, it’s raison d’être is to build and sell houses, then hand the profits from the sale of those properties back to the parent company so that it can build more social units for rent.

It may be worth mentioning – by way of background information – that before a name change in the first quarter of 2012 Mill Bay Homes was known as Pembrokeshire Housing Two Thousand Ltd, a company set up in 1998 that never traded.

So that’s the theory, the justification for Mill Bay Homes. But how’s it working out in practice? Let’s look at what information is available, add a few things that have been said, and then let us draw some conclusions, which we are fully entitled to do, as members of the generous Welsh public that has poured tens of millions of pounds into Pembrokeshire Housing.

When it comes to available information, we encounter a major obstacle in that it’s probably easier to get hold of Vladimir Putin’s personal e-mails than it is to see accounts for Mill Bay Homes. The problem being that because it’s not a regular company there’s nothing filed with Companies House. Because it’s not a charity it’s ditto with the Charity Commission. And while MBH claims to have filed accounts with the Financial Conduct Authority, the FCA says it has received nothing since the report for y/e 31.03.2013.

Though when my collaborator Wynne Jones wrote to the ‘Welsh’ Government, using an FoI request to ask for those accounts he was told, by Ceri Breeze, Head of Housing Policy, that the accounts were already in the public domain – with the Financial Conduct Authority! Sometimes it’s difficult to avoid the suspicion that information is being deliberately withheld on Mill Bay Homes, and that fibs are being told in order to throw people off the scent.

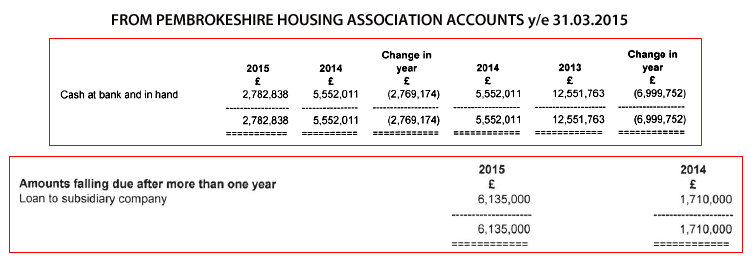

Anyway, let’s see what we can glean from the Pembrokeshire Housing accounts. In particular, the extracts below taken from the figures for the year ending on March 31st 2015. Figures that I suspect are connected.

You will see that between 31.03.2013 and 31.03.2015 Pembrokeshire Housing’s cash reserves fell dramatically, from £12,551,763 to £2,782,838. A reduction of £9,768,926, or 78%.

During the years ending 31.03.2014 and 31.03.2015 £6,135,000 was ‘loaned’ to Mill Bay Homes. The most recent figures available for Mill Bay Homes, those for y/e 31.03.2013, show a ‘loan’ of £245,000, which we can be fairly sure came from the parent company. If we add them it gives us a total of £6,360,000.

Without wishing to over-egg it I suggest we must also add other costs not stipulated. For example, Pembrokeshire Housing staff must have been working on the Mill Bay Homes ‘project’, and they must have used Pembrokeshire Housing offices and equipment, plus consumables, before Mill Bay Homes was up and running.

So I think we can reasonably assume that Mill Bay Homes owes Pembrokeshire Housing closer to seven million pounds than six. How is this to be repaid? Fortunately, last week’s Pembrokeshire Herald ran an article on my recent, ahem, difficulties and in this article group supremo Peter Maggs was quoted as saying, “The target is (for MBH) to deliver £1m of surplus for each of the next five years”. Which will – if achieved – return just five of the six million plus that’s owed.

(Note that the Pembrokeshire Herald couldn’t get my name right – “Roytston”, they called me, bloody “Roytston”!!! Is that defamation? Maybe I need a good solicitor – I wonder if Ms Singlehurst-Ward would take the case?)

‘A MILLION A YEAR FOR FIVE YEARS’, SAYS YER MAN

I have no opportunity to buy the otherwise excellent Pembrokeshire Herald except when I’m visiting the county, so I haven’t seen the ‘paper myself. But someone was kind enough to send me a photograph of the article, here, and another kind act saw the piece sent as text.

{kind=link}

Seeing as we are talking of Mill Bay Homes repaying Pembrokeshire Housing a cool million a year it might be instructive to know if any of the outstanding six million plus has yet been repaid. The figures for y/e 31.03.2016 are obviously not yet available, but the previous year’s figures tell us that the princely sum of £36,070 was received. Which leaves . . . roughly the same figure we started with. And that’s without taking interest into account.

Another way of looking at it would be that at the rate of £36,070 a year it would take Mill Bay Homes 176 years to repay what it owes.

This might make some of you think that Peter Maggs’ claim is a little overblown, but it could be worse than that. Here are a number of things to consider:

- I’m told that Mill Bay Homes is working to a 17% profit margin while the building industry usually works to a 25% margin on new builds.

- Before anything can be returned to Pembrokeshire Housing Mill Bay Homes will have to deduct its costs. In addition, it will need to buy the next development site and go through the planning process and other procedures, then pay to build that next development.

- So how much from each house sale will Pembrokeshire Housing actually see? Let’s assume that the average sale price of a Mill Bay property is £130,000. At 17% and deducting the costs just mentioned Pembrokeshire Housing might see a return of £50,000 per property.

- Of course, these calculations are necessarily speculative due to the absence of any publicly available accounts or other information for Mill Bay Homes.

- If the purpose of lending money to Mill Bay Homes is to generate income to build social housing why didn’t Pembrokeshire Housing instead of lending the money to get part of it returned use all of it to build social housing?

INTERPRETATIONS

One worry I have is that achieving Peter Maggs’ target will result in unfair competition for local building firms without the benefit of Mill Bay Homes’ inexhaustible source of funding, a source that relieves it of the need to return a profit. Is this the plan?

‘Welsh’ Labour we know is anti-business, also a ‘statist’ party that wants to control everything. So is this its way of surreptitiously making house building a state-controlled industry? If not, how else do we explain a publicly-funded housing association being allowed to set up a subsidiary that is, effectively, a no-risk private house builder?

One possibility is that we are discussing a trailblazer for a new type of business entirely. This is not idle speculation on my part, the idea has been knocking around for a while. I’m talking now of fully privatised housing associations. And it’s already started, as this article from the Guardian last August tells us.

The advantages are obvious. Housing associations have solid assets in the form of bricks and mortar, so they’ll have little trouble finding investors and securing loans. As long as the right legal safeguards are in place for all types of tenants, and the right incentives for investors, why not relieve the public purse of a massive burden by privatising social housing in Wales? These could be lucrative, profit-making businesses.

Proven by Pembrokeshire Housing itself. In 2013 it had cash reserves of £12,551,763, yet it’s one of the smaller housing associations, this is partly due to the fact that Pembrokeshire County Council retains its own council housing stock. If such a small outfit can build up such cash reserves then what is the picture with the big boys?

Though that said, some people – more cynical than I, you understand – might suggest that Mill Bay Homes was set up for the express purpose of soaking up this embarrassment of cash. For the nest-egg might otherwise have had to be returned, or might have resulted in reduced funding. Because I’m sure most people would believe that a relatively small, rural housing association with over £12m stashed under the mattress should not be receiving a penny from the public purse.

One thing’s for sure, housing associations as we know them in Wales are discredited. For a start, there are just too many of them, receiving inordinate amounts of funding, with too much of that money going on inflated salaries and administrative costs, and with very little effective oversight by the ‘Welsh’ Government. Housing associations are out of control, like some over-indulged adolescent forever finding new ways to get money out of his parents.

In addition, and perhaps especially in rural areas, housing associations waste money on new properties for which there is no local demand, then they import tenants, many of whom have ‘issues’, because of course they can charge more for housing problem families, petty criminals, drug addicts and other undesirables than they could ever charge hard-working, law-abiding locals.

Unless I receive important new information on Pembrokeshire Housing and Mill Bay Homes this may be my final post on the subject. I think I’ve said everything I need to say at present.

If those who claim to be managing Wales still see nothing wrong with the parent – subsidiary arrangement I’ve described, and if they believe that the current plethora of publicly-funded and competing housing associations is the cheapest and most effective way of delivering rented accommodation, then Wales is in a bigger mess than I had ever imagined.

UPDATE 17.06.2016: Surprise! Surprise! After all the attention Mill Bay Homes has been getting of late the Annual Return and Accounts for y/e 31.03.2014 and y/e 31.03.2015 are finally available on the Financial Conduct Authority website. They were added just a few days ago.

As I’m tied up for the next few days I won’t have time to give these accounts the attention they deserve, but perhaps my analytical readers would like to peruse them and give us their interpretations. Here are the accounts for 2014 and here for 2015.

Quickly skimming through them I was struck by the fact that in the 2015 report, in answer to question 1.19, Mill Bay Homes claims to be a Community Benefit Society because it benefits, “People seeking housing accommodation” (as opposed to any other form of accommodation). If Mill Bay Homes is accepted as a Community Benefit Society then I suggest the FCA gets ready for a rush of applications to join the club – from Wimpey, Persimmon, Redrow and all the rest.

But of course MBH would defend its claim to be a Community Benefit Society by the answer it gives to 1.21, which asks how surpluses or profits are used. The answer reads, “Surplus was transferred to the parent Registered Social Landlord to invest in affordable housing”. Why not just say ‘the parent company’, why stress that it’s a RSL? And why “affordable housing” not ‘social housing’? MBH claims to build and sell ‘affordable housing’.

Though these considerations bring us back to the underlying idiocy of this model. Pembrokeshire Housing, a provider of social housing, has £10m in spare cash. Rather than use that money for the purpose it was given the money is loaned to Mill Bay Homes to build and sell houses. Then perhaps £1m of profit is returned to PH for social housing. Why not use the original £10m for its intended purpose of social housing?

Could it be that Pembrokeshire Housing had more money than it needed, or knew how to use, and rather than admit to that embarrassment, it came up with the absurdity that is Mill Bay Homes?

UPDATE 21.07.2016: In an e-mail of July 18th Simon Fowler of the ‘Welsh’ Government’s Housing Directorate, had this to say: “We have had sight of a confirmation from the FCA that Pembrokeshire Housing and Mill Bay Homes submitted all their regulatory returns by the given deadline. It went on to confirm that due to an error at the FCA, the returns were not published. We are satisfied that PHA and MBH have not acted inappropriately – either deliberately or mistakenly – when submitting the returns required by law.”

Today, my co-investigator, Wynne Jones, received an e-mail from Nazmul Ahmed at the FCA, he had this to say of the Mill Bay Homes returns: “I have spoken to my colleague and we can provide the dates we received the annual return and accounts – 2013/14- 2 June 2016, 2014/15- 2 June 2016′.

The timing is significant. I published posts on Mill Bay Homes on the following dates, April 25th, May 20th and May 23rd. These were taken down under threat of legal action conveyed in a letter from Ms Tracey Singlehurst-Ward of Hugh James Solicitors of May 31st. I can imagine Ms S-W saying to MBH, ‘OK, I’ll try and put the frighteners on him, but you’ve got to get your house in order, don’t give him ammunition’.

But where does this leave Simon Fowler? I think the kindest thing I can say of Mr Fowler and his colleagues is that they make it up as they go along. What I and others have learnt in recent months suggests there is no oversight of housing associations by the ‘Welsh’ Government, little regulation, and that they are free to do as they like – with hundreds of millions of pounds of our money.

~~~~~~~~~~~~~~~~~~~~~~~~~ END ~~~~~~~~~~~~~~~~~~~~~~~~~

NEXT: The promised article in which I explain why I’m voting Leave in the EU referendum

I am buying a plot of land in the coppins in pentlepoir one which millbay homes didn’t buy my intention is to build three terraced houses but I have to pay £12675 per house that’s over 38k as a small builder this is madness when millbay homes is making millions in profits not giving back to social housing

Having examined MBH accounts for 2014 and 2015 your attention is drawn to a subtle change of wording in their reply to question 19 Group Structure. In 2014 accounts they confirm that “the company is a subsidiary company of Pembrokeshire Housing Association Ltd.” In 2015 accounts they confirm that “the company is a wholly owned subsidiary company of Pembrokeshire Housing Association Ltd”

In reply to question 16 Development Commitments, they confirm development expenditure that has been contracted for but has not been provided for in the financial statements and which will be funded by loans from the parent company. These are as listed below.

2013 £589,949

2014 £5,388,382

2015 £6,989,561

In my view the interesting question is whether the loans were provided on commercial terms as required under Welsh Government circular RSL 05/08 Group Structures, and whether social housing grant allocated to the parent company to deliver social housing in Pembrokeshire has been transferred to the subsidiary to fund the purchase of open market development sites at Letterston, Pentlepoir, Templeton Crundale and Cilgerran.

In 2015 accounts the following information is provided in response to questions on form.

Question – Who are the community the society benefited?

Answer – People seeking housing accommodation.

Question – How did the society benefit that community during the year?

Answer – The society provided housing accommodation with associated facilities and amenities.

Question – How did the society use any surplus / profit.

Answer – Surplus was transferred to the parent Registered Social Landlord to invest in affordable housing.

I shall leave it to others {who are more suitably qualified} to comment on whether these statements are appropriate for a community benefit society. The parent company should not be investing in “affordable” housing it should be investing in “social” housing. There is an obvious difference.

Thanks for the update Jac. There is a distinction between “social” housing and “affordable” housing. I have examined a copy of the signed S.106 agreement between Pembrokeshire County Council and Mill Bay Homes relating to the development at Ashford Park Crundale Haverfordwest. Planning Permission was granted for 62 dwellings. Under the terms of the S.106 agreement, Mill Bay Homes agreed to provide 12 “affordable” housing units, 11 of the affordable units to be sold as social rented housing units to the parent company or offered for sale to Pembrokeshire County Council under certain circumstances. Under the terms of the agreement, the remaining 1 intermediate housing unit is to be offered for sale at 70% of open market value. A copy of the signed agreement can be made available to anyone wishing to examine the provisions in more detail.

It remains unclear whether social housing grant provided by Welsh Government to the parent company has been transferred to the subsidiary company to fund the construction of these 11 “affordable” housing units.

Is there a possible conflict of interest here between the Council’s regulatory planning role in granting planning permission for the development while also being in a position to purchase some of the properties under its role as housing provider.

Some years ago I tried to get an official definition of ‘affordable housing’. It can mean whatever the person using the term wants it to mean. It is a very elastic term.

THE FOLLOWING COMMENT WAS RECEIVED ANONYMOUSLY BY E-MAIL.

On the subject of problem accounts, it is worth noting that Mill Bay Homes sub-contracted the Pentlepoir development to Hale Construction, a family owned business in Neath. Hale Construction supplied the infamous Tom Whelan, the Irish Site Manager who ‘returned’ to Ireland owing over £1000 in rent, Lee Sinclair provided the ‘digger’ and the ‘muscle’ for the infamous swinging digger arm incident. A similar set-up, apart from Tom Whelan, is also being used at the recently commenced Kilgetty site.

So what is my point? Well, Mill Bay Homes Ltd are not the only ones having problems providing accounts, as can be seen from the Companies House extract below, which shows that Lee Sinclair are facing an ‘Active Proposal to Strike Off’.

https://beta.companieshouse.gov.uk/company/07707053

it seems to me that while I’ve been focused on Mill Bay Homes building private housing in order to subsidise the affordable homes of Pembrokeshire Housing (for rent for older persons, familes and single persons as well as people with support needs – it says on their website), it may have been the other way around. If PH has “loaned” MBH over £6 million for it to carry out its business then just imagine how many more affordable homes it could have built with that money for those sections of the community who have a genuine need. Buyers on MBH developments can presumably afford to pick and choose houses off any private development.

A very good point, and one that I had planned to make – but forgot.

The only justification I think PH could come up with is that by loaning money to MBH it helps first-time buyers. Unfortunately this defence is undermined by MBH advertising for investors and retirees. And how many local first-time buyers can afford – or need – a four-bed detached property?

Something else that I wonder about is whether Pembrokeshire Housing couldn’t have built properties for sale under its own name.

A couple of good posts already and the last point by Brychan is particularly apt i.e. ‘ just publish their ‘wonderful returns for social purpose’.

I think the Pembrokeshire Herald article is a strange move by Peter Maggs but nevertheless politically interesting. I have met all the people in the photograph, that is included with the article, but I have only ever conversed with Peter Maggs via e-mail and I have my own personal views about all of them. Both Peter Maggs CEO and Nick (Nicky) Garrod Land & Construction Manager are, in ‘my personal opinion’ (in case Ms Some-Body is reading this) political operators, with traits reminiscent of the film character Robert Ritter (CIA Politico) up against agent Jack Ryan (played by Harrison Ford) in ‘Clear and Present Danger’, see slightly modified extract from script as follows:

“I have an autographed get-out-of-jail-free card! ‘The President of the United States of Wales authorises CEO Peter ‘Ritter’ Maggs to conduct ‘Operation Mill Bay’ including all necessary funding and support. This action is deemed important to the national security of the United States of Wales etcetera, etcetera, etcetera’ You don’t have one of these, do you Jac? [as Jac blogs away] Grey! The world is grey, Jac!”

In the Herald article Peter Maggs clearly does the hard sell but he also plays his ‘get-out-of-jail-free-card’ where he states that he had the approval of the Welsh Government with regard to the creation and activities of Mill Bay Homes Ltd. I wonder if anyone is able to produce evidence of such approval and oversight from our political masters?

Jac – As always you have cast your bright light over the ‘grey’ and revealed to us what lurks in the shadows – I hope for all our sake that you have got a ‘Get-out-of-jail-free-card’!

Not having seen that movie I’m afraid the reference is lost on me. Though he may be right about ‘Welsh’ Government approval. Mill Bay Homes may even have been a ‘Welsh’ Government initiative.

Look at it this way: A relatively small, publicly-funded, not-for-profit organisation builds up cash reserves of £12.5m. This does not look good, for the organisation involved or for those funding it – the ‘Welsh’ Government. So rather than have the money returned, or future funding cut (both of which might cause embarrassment), someone in Cardiff could have said, ‘Come up with a

scamscheme to soak up your cash reserves’.Just a thought.

Actually, the ‘Welsh Government’ does not really exist. Civil servants in Cardiff were just dishing out ‘what’s allowed’ advise on a speculative punt. The AMs haven’t got a clue and the minister at the time would not have been able to add up his pie shop receipt. I don’t think the civil servants in Cardiff would have run it over the ministers desk, they are more likely to just ask their superiors in Whitehall for reassurance, who would, in turn, have seen £12.5m as small beer. At the same time the ‘social entrepreneurs’ of the local golf club would have been well aware that if you buy a few acres in Pembrokeshire with odds-on of getting planning permission, you can’t lose. Sort out the corporate governance issue later, get the buy-build-sell ball rolling, and keep the ball rolling by sniffing out farmers with scraps of land to sell. The cash being punted is taxpayers money, and if it fails Auntie Flo lives with damp a few more years and you still get to Pimms it up on the Cleddau. Call me an old cynic.

This is a point I have consistently made in this blog – the ‘Welsh’ Government is just window-dressing for the civil servants who really run the show, and take their orders from London.

With regard to the formation of Mill Bay Homes in April 2012, it would appear that we have a statement from Mr Peter Maggs published in the Pembrokeshire Herald that they were given the “all clear” from Welsh Government. Correspondence with Welsh Government is continuing to establish what formal consent was granted. A key document would appear to be “Housing Association Circular RSL 05 / 08 Group Structures.” The circular takes effect from 1 October 2008. The paragraphs considered relevant to the Pembrokeshire Housing Group are reproduced below.

3.4

Proposals for new group structures or changes to existing group structures will require written approval by the Welsh Assembly Government {the Assembly Government}. Existing lenders should be consulted. When seeking Assembly Government approval an RSL will need to provide a business case that demonstrates the specific benefits the proposed group structure will achieve and that the short term costs of establishing or changing a group structure are outweighed or at least balanced by longer term efficiency gains.

4.1

The regulatory returns and annual accounts of RSLs must make clear all horizontal and vertical relationships with other group members. All intra-group movements of resources, including any collateral liability, equity investments, loans and on-lending must be disclosed.

4.2

RSLs should make clear to their lenders the status of the entity with whom they are dealing and their relationship with other members of the group.

4.3

Each RSL within a group must be independently financially viable.

5.2

A non-registered subsidiary must be a separate legal entity from a registered parent and other registered members of a group.

5.4

All financial and contractual arrangements between an RSL and an unregistered subsidiary must be at arms-length and any loans or investments must be on a commercial, secured basis.

5.5

All intra-group transfer of funds or assets must be clearly shown in the accounts of the parties, which shall be made available to the Assembly Government.

6.4

Shared accommodation

One company {preferably the parent} should own the premises and make suitable charges for the accommodation used by other organisations. Use of the accommodation should be subject to a formal agreement, which sets rental charges at commercial terms. Where offices are shared, different companies should have different telephone numbers and calls should be answered in the name of the company and not the group.

6.6

Services bought and sold

Services bought from an unregistered subsidiary must demonstrate value for money. Services sold to an unregistered subsidiary must be subject to a formal agreement and be on a basis that at least fully covers costs. Any equipment or other asset purchased by a parent {or other registered group member} for use by an unregistered subsidiary should be leased to the subsidiary on terms that earn income at least equal to commonly available market investment rates.

6.7

Accounting records and documentation must always show clearly to which company they relate, and to which company they belong. Where the parent provides accounting services to the subsidiary it is particularly important that decisions about the content of the subsidiary’s accounts, and especially their approval, are clearly seen to be decisions of the subsidiary.

It would have been impossible for Mr Maggs to get the ‘go-ahead’ from the Welsh Government in 2012 or been guided by the 2008 guidance notes. The Act of Westminster parliament that governs the structure created was not given royal assent until 2014. It was part of the ‘Big Society’ chunk of legislation from London.

I’ve looked at other Housing Associations and have found none in Wales similarly structured. Valleys is ample cheap housing stock, Cardiff has overheated and full of normal private developers wanting to build on sites like Caerffili mountain. The strange thing about Pembrokeshire is that it has a pocket of poverty and cheap run-down housing stock in Milford Haven and Pembroke Dock. An area which has ample brown field land for development, but the money is made furnishing demand is for holiday homes and retirement palaces around Saunderfoot and green-field heaven up on the Ceredigion border. The PH and MBH structure is an instrument to get cash subsidy from the Welsh Government to corner the market for posh developments. This money was supposed to help house the indiginous poor, but it’s actually being used as leverage to house posh incomers. I doubt even the Labour champagne socialists of the Bae saw it coming, unless they’re in on it.

.

Yes, I agree Brychan. Thanks to Jac, and those that contribute to this blog with very helpful comments, there is now a mountain of evidence available in the public domain. Time for this nonsense to end and for public funds to be managed in a proper manner and for housing associations to be accountable to the taxpayer who part fund their projects. Self-regulation needs to be replaced with proper regulation.

Seeing as how you have had the jackals and hyenas set upon you, it is worth recalling Dick’s memorable line from Henry VI, Part 2, Act 4, Scene 2.

Nay, say it I mean not to do.

Thanks again Jac. Another well researched and very informative and helpful post. In view of your observations, I shall be examining very carefully every word in Ceri Breeze’s response to my request for information.

I suspect that over the years Mr Breeze has had his finger in many pies . . . and not all of them made by the Thomas brothers.

If a HA registered as an IPS accumulates a large capital surplus what is it to do with it? They exist in a sort of legal/ideological limbo between a commercial company and a charity. They are supposed to plough back most of their surplus into providing housing, maintaining existing stock and possibly providing facilities for their tenants. Unlike a commercial company they can´t simply hand out bonuses to their shareholders. And the interest they´re allowed to pay on their shares and loanstock is limited. This is a bit of a grey area but generally a few percent per annum, so they can´t just whack that up to distribute the goodies. They might of course inflate the salaries they pay to employees. But that would have to get past the board and ultimately the AGM. So who actually controls this outfit? Who are it´s members/shareholders who ultimately rubber-stamp all decisions? With an IPS this is a lot harder to find out than with a Ltd. Co.

(Hope this is helpful, I´ve only ever dealt with tiny co-operative housing assocs, but the basic legal and admin set-up is the same I think)

So good luck and keep digging, no smoke with fire etc.

Floatie.

The reason why Pembrokeshire Housing Association is also registered as a Community Benefit company is so that it can bank a “floatie”. The subsidiary, Mill Bay Homes cannot have an institutional ownership of more than £100k, in value, unless it’s parent is also registered as such (32). The parent gets rewarded via a floating surplus.

Latest annual return.

Any financial surpluses from Mill Bay activity cannot be fed up to the parent unless there is a fixed or variable (floating) charge. It is not a ‘covenant’ as has been wrongly described. See my comment above. Mr Maggs has already confirmed that the amount is variable by year (floating) and also that the amount is circa £1million for the year 2015/16 in his statement to the Herald (59). This means that activities for the year ending March 2016 has crystallised and the (can be yet to be audited) balance sheet must be available, and also notice of this transfer made to the FCA (61).

Statutory obligations.

This means that (a) the balance sheet is NOW available for inspection by the public at the registered office for year ending March 2016, and this must be displayed ‘conspicuously’ according to the 2014 Act (81 and 98), and (b) any borrowing and charges upon assets of the parent company also has to comply with the 2014 Act. This explains the entries of charges from the Pru and the Prince registered with the FCA (59).

Link.

http://www.legislation.gov.uk/ukpga/2014/14/contents/enacted

I was wondering why the first reaction of PHA and MBH was to find an expensive lawyer rather than go down the public relations route (which it is now doing). It’s because going public results in the full revelation of the business model and current arrangements.

If Mill Bay Homes is “a business with a social purpose, and they state “the fact that earnings will be covenanted to the parent company (Pembrokeshire Housing) for the express purpose of re-investment in the affordable housing.(sic)” then hey should have no problem, whatsoever is stating what amounts have already been covenanted since 2013 on this statement on their website.

This is especially the case as they boast that almost all the properties built by Mill Bay Homes in various sites in Pembrokeshire have now been sold. If the business model is such a wonderful philanthropic enterprise, then surely they should be shouting this from the rooftops? We can only speculate why no figures are available.

The Financial Conduct Authority are currently reviewing their accounts up to end March 2014 and state they do not have their accounts up to end March 2015. My speculation is that (a) there are in fact no profits to be covenanted as it is a failed enterprise, and/or, (b) there are still outstanding costs to be incurred on properties that have been sold such as unsatisfied section 106 agreements, and/or (c) outstanding costs to be incurred on the quality of properties that have been sold such as remedial works to satisfy NHBC certification.

Obviously, if and when Mill Bay Homes do provide some numbers on the ‘amounts covenanted for social purpose’ is would then be possible to determine the yield. This ‘yield for social purpose’ is currently available for normal enterprise housing developments, for example, Persimmon who have new build developments along the M4 corridor, where there is real and evident housing demand, and have already paid over large sums for social purpose in the construction of social amenity.

Why does Mill Bay Homes resort to defamation lawyers to hound bloggers rather than just publish their ‘wonderful returns for social purpose’, which they claim?

Note – A ‘positive’ covenant (as apposed to a restrictive covenant), is corporate finance, must satisfy all three conditions…

(a) it must not be personal in nature and must benefit something physical such as land or houses rather than an individual or other corporate entity, and (b) must ‘touch and concern’ the enterprise and it must affect how the asset is used or the value of the asset held, and (c) the benefit must be identifiable.

It is also a reason why such covenants “cannot be a positive burden”, so once crystallised, it must not require further expenditure to meet it. The statement by Mr Maggs, the CEO of Pembrokeshire Housing to the Pembrokeshire Herald is meaningless, as he has used the word ‘target’ in his statement.

This either means that the ‘covenant’ does not yet exist, or that it’s value has not yet crystallised, or it’s use not physically present.

Another eye-opening article, Roytston (couldn’t resist…!).

Two small things about the accounts, though:

I take it that the “loans” item is in the balance sheet. In which case the figure shown is the total owed at the end of the year. In other words, during 2015, PH must have lent an additional £4,425,000 to the subsdiary to bring the total up from £1,710,000 to £6,135,000. Still eye watering amounts, mind!

Also, the income item must be in addition to repayment of loans. Whatever income is paid from the subsidiary to the parent, the loan should remain the same unless there are additional payments or re-payments. These probably wouldn’t be itemised – they’d just show up as an increased or decreased figure, although there may be a breakdown somewhere in the notes.

It’s not unreasonable for a housebuilder to have £5 or £6 million of loan capital – for land-bank, building costs, unsold properties etc, and you never know, if the company are able to use the Parent’s planning clout, office resources, in mouse maintenance team etc, then they might be able to turn a tidy profit.

All at the expense of other, local builders, as you point out.

I shall make the adjustment.